Tariff Day Takeaways

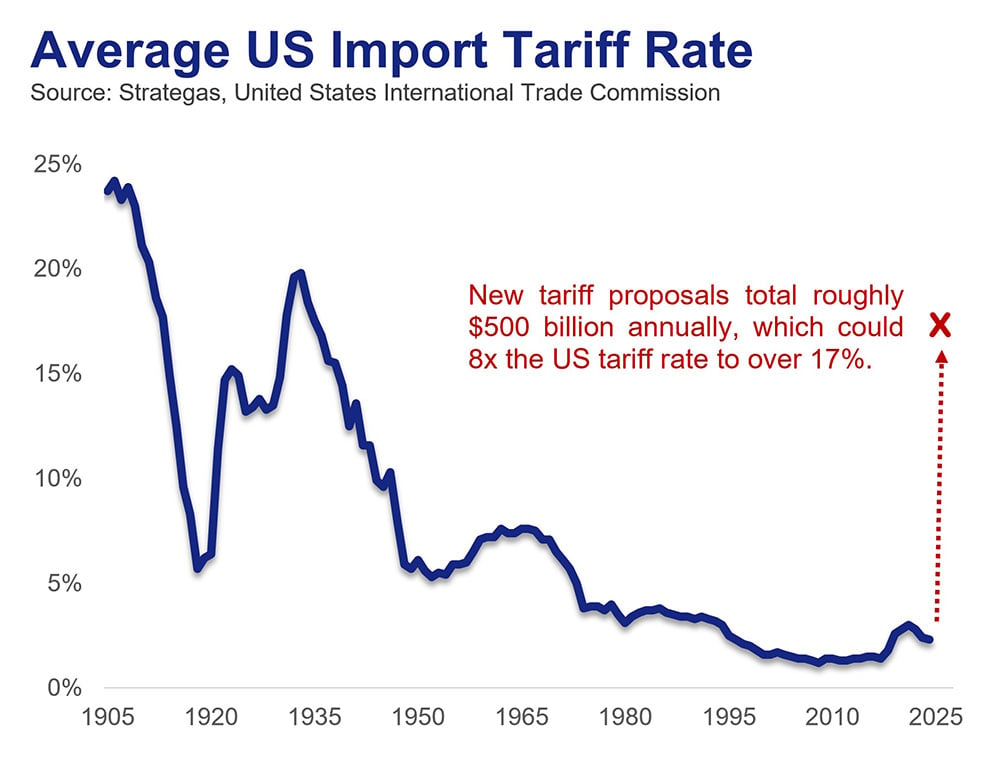

Trade uncertainty has rattled investors, consumers, and businesses to start 2025. On April 2, President Trump announced his complete tariff proposal, which we believe is near the worst-case scenario. We estimate the plan will generate roughly $500 billion of tariff revenue on top of what has already been enacted. Below, we give some quick thoughts on the events.

While we expected President Trump to make tariffs a key pillar of his policy agenda, the sheer size of the tariffs, coupled with the (thus far) haphazard implementation plan, has created market turmoil and made it difficult for companies to plan for the future. On April 2, President Trump announced a comprehensive tariff framework, which we believe is near the worst-case scenario. We estimate the proposal will generate roughly $500 billion of tariff revenue on top of the $150 billion that has already been enacted. President Trump said he wanted $500 billion, and he got it. This represents 2.2% of GDP and is twice the size of the largest tax increase in modern US history. What follows are some facts and quick-hitting takeaways from the proposal:

- The main basis of the plan is a 10% universal tariff rate. For countries with larger trade deficits and/or high tariff rates, the US will impose even higher rates above the 10%.

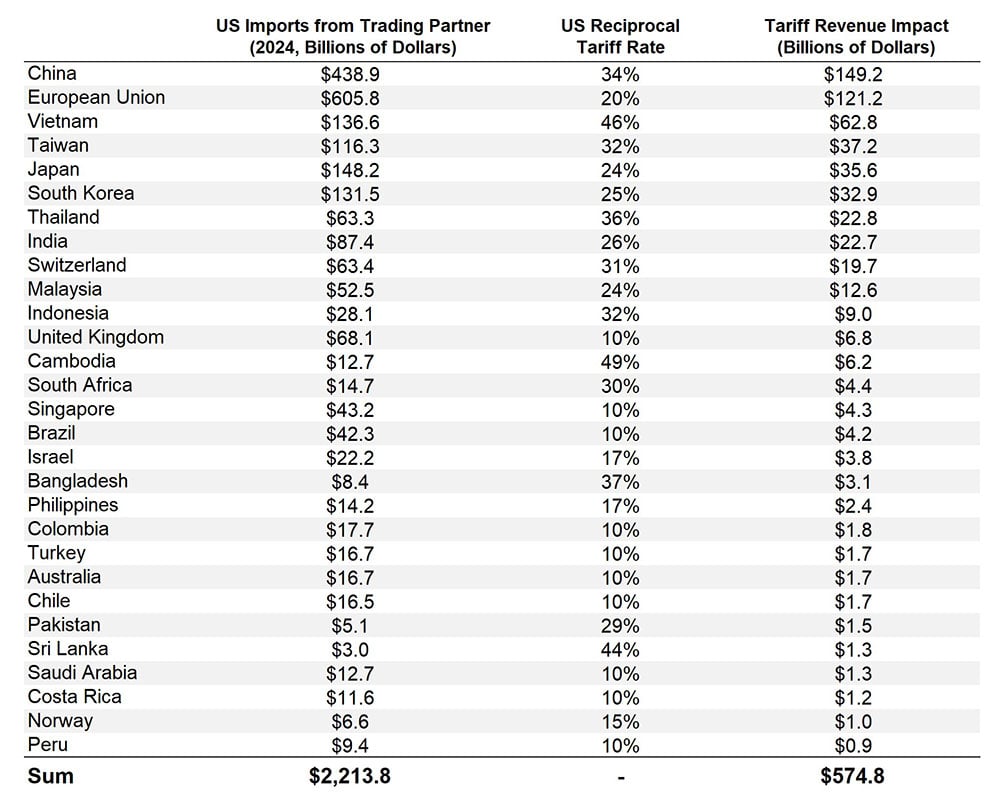

- The rates will exceed 10% for 58 countries and every import from the EU will face a 20% rate. Some of the rates are so high, the proposal is hard to believe. Our back-of-the-envelope calculation suggests that Vietnam will face tariffs of more than 10% of GDP.

- Trump is near his campaign proposal of 60% China tariff rates. Under the new proposal China will be hit with an additional 34% tariff rate. This is on top of the 20% already enacted, raising the total to 54%. Trump also eliminated the de minimis exemption (a provision which allows companies to avoid import taxes on international shipments with a retail value of $800 or less).

- Mexico and Canada are relative winners under the new plan. Mexico and Canada will not be subject to the 10% tariff. The existing 25% tariff on non-USMCA compliant goods will remain in place.

- The rates came in higher than the consensus expected. US allies are facing high tariff rates, such as Japan (24%), South Korea (25%), Vietnam (46%), and Taiwan (32%).

- The foreign policy implications are enormous. These tariffs are so large that the economic implications may not be the only impact. There will likely be foreign policy implications and non-US countries are likely to shun US products and companies moving forward.

- Congress now has the revenue to lower corporate and individual income tax rates. The April 2 proposal is roughly a doubling of the corporate tax rate. With this new revenue source, Congress will need to deliver on a large tax cut to sterilize the negative impact of higher tariff rates. This must be bigger than just 100% expensing of capital goods; it needs to be large-scale tax rate reductions to help soften the economic blow.

- These tariffs were enacted under the International Emergency Economic Powers Act (IEEPA) and will likely face a legal test about whether IEEPA can be used for such sweeping tariffs by executive action.

- A sharp negative market reaction should catalyze Congress to move closer to getting a tax bill completed. The House and Senate remain at odds over the level of spending cuts. Our sense is that some of these issues will be worked out in the coming weeks to get the tax bill into effect quickly given the negative impact of the tariffs.

- We expect the US budget deficit to come down sharply in the short run. March looks to be an $80 billion deficit reduction month and we see it as the first sign of the deficit coming down from April tax revenues. The tariffs will only add to that, and the deficit will come down faster than the consensus expects. As such, there will be a downward adjustment of Treasury issuance, even if a portion of the revenue is used for tax cuts.

Source: Strategas, Census Bureau

Appendix – Important Disclosures

Past performance is not indicative of future results. This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent.

This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. Unless otherwise cited, market and economic statistics come from data providers Bloomberg and FactSet. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry or security. Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client. Investment involves risk. You should review the prospectus or other offering materials for an investment before you invest. You should also consult with your financial advisor to assist you with your analysis, risk evaluation, and decision-making regarding any investment.

The performance and other information presented in this communication is not indicative of future results. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies. Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication.

Strategas Securities, LLC is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses. A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at http://www.rwbaird.com/research-insights/research/coverage/third-party-research-disclosures.aspx. You can also call 1-800-792-2473 or write: Baird PWM Research & Analytics, 777 East Wisconsin Avenue, Milwaukee, WI 53202.