Market & Policy Mid-Year Outlook with Strategas

Strategas partners Nicholas Bohnsack and Dan Clifton address some pressing questions investors face heading into the second half the year. In the note below, they address inflation, recession, portfolio positioning, policy changes, midterm elections, and more.

KEY QUESTIONS FOR THE BACK HALF OF 2022

How are you evaluating the current investing landscape?

As we look out through year-end, we have to consider that there is a fair amount of uncertainty with respect to the economic outlook. If anything has surprised us, it's been how delayed investors have been in coming around to the view that it's going to take much more from policymakers to curb the effects of inflation. There's almost a complacency in the market, which is perhaps driven by an expectation for market activity to be V-shaped, when, by our lights, a market bottom is much more of a process. To get there, it's likely going to take an expectation reset around fundamentals, as well as an anchoring of inflation expectations. And those are tough hills to climb.

How are you thinking about odds for a recession over the next year, and what does that mean for corporate earnings?

An interesting thing about this environment is that, given the policy support that the government and the Federal Reserve have provided to the economy over the last number of years, handicapping recessions is much more difficult. There are clear pockets of strength in the US economy – most notably the labor market – and so it's very likely that, while we see an imminent slowdown in growth, jobs will remain plentiful enough that we might actually almost need a second recession in 2023 or 2024 to fully curb inflation. And the knock on effects for companies are very challenging. Revenues might remain elevated (in part due to inflation, i.e., the money illusion), but profit margins begin to come under very acute pressure as costs rise. And to the extent to which the labor market remains strong, the cost of labor continues higher and that's not really a good recipe to thwart inflation. So, we would anticipate profit margins will decline in the coming months and years.

An interesting thing about this environment is that, given the policy support that the government and the Federal Reserve have provided to the economy over the last number of years, handicapping recessions is much more difficult. There are clear pockets of strength in the US economy – most notably the labor market – and so it's very likely that, while we see an imminent slowdown in growth, jobs will remain plentiful enough that we might actually almost need a second recession in 2023 or 2024 to fully curb inflation. And the knock on effects for companies are very challenging. Revenues might remain elevated (in part due to inflation, i.e., the money illusion), but profit margins begin to come under very acute pressure as costs rise. And to the extent to which the labor market remains strong, the cost of labor continues higher and that's not really a good recipe to thwart inflation. So, we would anticipate profit margins will decline in the coming months and years.

Could you talk about why Strategas’ estimate for 2023 earnings is lower than consensus?

First, we really don't have as much confidence in the ability of companies to maintain previous levels of sales in a slowing economy, nor in their ability to pass on rising costs to the end consumer and keep profit margins elevated. That simple calculus conspires to send overall earnings lower and explains how we find ourselves with a lower-than-consensus estimate. We also haven't yet seen much downward revision from analysts in their forward earnings and profit margin estimates. They continue to have lofty expectations for 2022 and 2023, but it's our suspicion that as earnings are reported over the coming months and there are some disappointing numbers, you might begin to see estimates start to start to move lower towards our projection.

How is Strategas positioning its portfolios for this environment?

I think you must begin with the likelihood that a recession is closer at hand than assumed, and with inflation being the overriding consideration for most investor. That argues for a more conservative portfolio construction. We have taken a bias toward Domestic equities over International (especially Europe) and Value over Growth. There are opportunities across market capitalizations, but more conservative positioning would generally lead investors to move up that spectrum. Thematically we favor “cyclical defensives,” where we're trying to take advantage of latent pockets of strength, notably the labor market, while being mindful that growth was pulled forward into last year and that the overall growth profile of the economy is slowing.

What is the current political and policy environment in Washington?

Since the 2008 Financial Crisis, we've argued that economic volatility is creating political volatility in the U.S., and that weaker economic growth is leading to higher political turnover. This has created more policy uncertainty, which has made it harder to seed new investment across industry (oil and gas, healthcare, etc.). Companies are worried about the rules changing every two years, and that stymies growth. Much of this has been compounded by the four transformational and nearly unprecedented events of 2020 (recession, pandemic, mass protests, and presidential election), which are now leading to big policy outcomes. Consider that the last time we had these four events happen in one year was 1968, and the aftermath of that saw massive policy shifts (the end of Bretton woods, the OPEC oil embargo, record inflation, war, etc.) Putting it all together there could be big policy changes in the future that investors aren’t used to.

How has the shifting environment affected your policy frameworks?

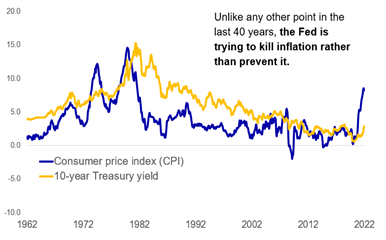

We have three major policy frameworks that we monitor – fiscal, monetary, and geopolitical – and this year all three were upended. First, monetary policy. Every interest rate increase since 1982 has been to prevent inflation, but for the first time in over 40 years (and with CPI at a 41-year high), the Fed is trying to dig inflation out of the system. This is a much more difficult job and will likely result in higher rates. Second, geopolitical policy. The most significant 2022 event so far has been Xi Jinping and Vladimir Putin at the Olympics saying they are going to change the world order. Russia-Ukraine is just a byproduct of this. And now historic events are flying by us in real time: Finland and Sweden trying to join NATO, Japan talking about NATO for Asia, etc. The shifting world order is heightening geopolitical uncertainty. Third, fiscal policy. Many investors expect that a recession would again lead to a big fiscal response, a la pandemic stimulus. But we don’t agree. US debt-to-GDP is at 120%, and there's concern at the federal level that handing out stimulus checks stoked inflation. This changes how the federal government might respond to recession going forward. All three policy frameworks have been totally upended. That's not a bearish outcome, but investors need to adjust to that changing framework.

We have three major policy frameworks that we monitor – fiscal, monetary, and geopolitical – and this year all three were upended. First, monetary policy. Every interest rate increase since 1982 has been to prevent inflation, but for the first time in over 40 years (and with CPI at a 41-year high), the Fed is trying to dig inflation out of the system. This is a much more difficult job and will likely result in higher rates. Second, geopolitical policy. The most significant 2022 event so far has been Xi Jinping and Vladimir Putin at the Olympics saying they are going to change the world order. Russia-Ukraine is just a byproduct of this. And now historic events are flying by us in real time: Finland and Sweden trying to join NATO, Japan talking about NATO for Asia, etc. The shifting world order is heightening geopolitical uncertainty. Third, fiscal policy. Many investors expect that a recession would again lead to a big fiscal response, a la pandemic stimulus. But we don’t agree. US debt-to-GDP is at 120%, and there's concern at the federal level that handing out stimulus checks stoked inflation. This changes how the federal government might respond to recession going forward. All three policy frameworks have been totally upended. That's not a bearish outcome, but investors need to adjust to that changing framework.

What are the legislative priorities ahead of the midterms?

Democrats are rushing to get as many policy victories as possible before the midterm elections. Top priority is passing a smaller version of Build Back Better. They have until Sept. 30 to pass this legislation on party line vote using budget reconciliation, but time is running out. We think final legislation will focus on four areas: 1) $600 billion of renewable energy spending (wind, solar, storage, nuclear, etc.); 2) Increased healthcare spending on Affordable Care Act subsidies; 3) A wealth surtax on individuals making over $10 million, a new 3.8% tax on small business income, a 15% minimum corporate rate, and higher taxes on US multinationals; 4) Something on drug prices in the Medicare system. A side goal is to raise more in taxes than is spent and claim that a lower deficit will reduce inflation. And while tax hikes have not historically reduced inflation, the argument is helping drive negotiations. It won't be easy, but if an agreement can be reached in the next few weeks, the process can move quickly.

What’s your midterm outlook, and what are the investment implications?

The president's approval rating is the single best indicator of seat losses for the incumbent’s party. President Biden's approval rating is 40–42% (similar to President Trump's 4 years ago), which is consistent with losing 30–40 House seats. This could change, but it's likely the Republicans will gain the 5 seats needed to win the House. The outcome is harder to predict for the Senate, but Republicans only need one seat to win, and we think they're probably going to pick it up. As for markets, we are often asked what the investment implication of a change in political parties might be. We would argue that just getting to the election – no matter who wins – has had a significant and positive effect for investors in midterm years. These years tend to be very volatile for stocks, with the S&P 500 declining by 19% on average (most of any year in a presidential cycle). However, the S&P 500 is up by an average of 32% one year from the midterm selloff bottom, and further, the S&P 500 has not declined in the 12 months following a midterm election since 1946. That doesn't mean it’s going to happen again, but we do believe in history. And in the past, the relief of simply getting to the election has been the catalyst for some of that outperformance.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry or security. Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client; therefore, this communication should be treated as impersonal investment advice. The intended recipients of this communication are presumed to be capable of conducting their own analysis, risk evaluation, and decision-making regarding their investments.

For investors subject to MiFID II (European Directive 2014/65/EU and related Delegated Directives): We classify the intended recipients of this communication as “professional clients” or “eligible counterparties” with the meaning of MiFID II and the rules of the UK Financial Conduct Authority. The contents of this report are not provided on an independent basis and are not “investment advice” or “personal recommendations” within the meaning of MiFID II and the rules of the UK Financial Conduct Authority.

The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies. Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication.

Strategas Securities, LLC is a registered broker-dealer and FINRA member firm, as well as an SEC-registered investment adviser. It is affiliated with Strategas Asset Management, LLC, an SEC-registered investment adviser. Strategas Securities, LLC is also affiliated with and wholly owned by Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses.

A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at http://www.rwbaird.com/research-insights/research/coverage/thirdpartyresearch-disclosures.aspx.

You can also call 1-800-792-2473 or write: Robert W. Baird & Co., PWM Research & Analytics, 777 E. Wisconsin Avenue, Milwaukee, WI 53202.